As the Reserve Bank of India (RBI) presses the pause button on rate hikes, investors must lock in fixed rate (FD) bank deposits at higher interest rates and select the duration according to their horizon of investment. Most banks currently offer fixed deposits with rates of 7% or higher. The interest rates of small financial banks are even higher than those offered by public and private sector banks and post offices.

Since diversification reduces risk to your investments, the FD portfolio should be spread across banks and various companies and among mandates. Hold deposits of various maturities, ranging from 180 days to more than five years.

Adhil Shetty, CEO of Bankbazaar.com, says there are several options with major banks and corporations that allow an investor to lock in peak rates for five years or more. “If you’re locked into a lower rate than last year, you can liquidate your FD and reinvest for higher returns,” he says.

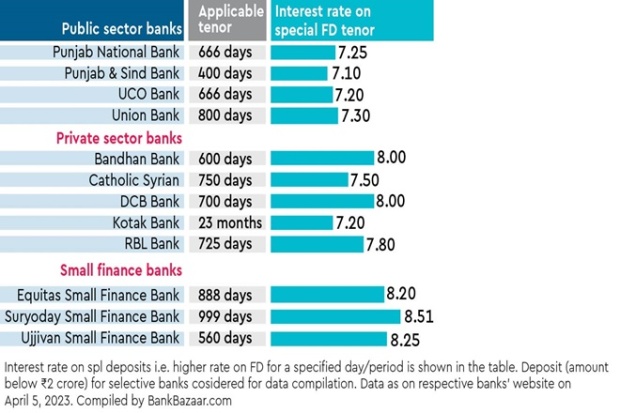

Many banks offer special term deposits with higher rates (See Yield Barometer). However, as these schemes do not allow early withdrawal facility, depositors should consider their liquidity needs before investing in special FD schemes.

The repo rate is not the only factor influencing the variation of FD rates. Naveen Kukreja, CEO and co-founder of Paisabazaar.com, says that FD rates are also influenced by the spread between credit growth rates and deposit growth rates and the overall liquidity of the system. As long as credit growth rates exceed bank deposit growth rates, banks would continue to raise their FD interest rates to attract more fixed deposits to meet the growing demand for credit.

Also Read: Personal Loan vs Loan Against Securities: Which is the Best Option for You?

While the pause in policy rate hikes may temporarily halt interest rate hikes on loans, the same cannot be said for FD rates. “Existing FD depositors should continue with their FD until maturity, regardless of changes in the repo rate. They should opt for a premature DF

close only if they find a significant gap between the new FD rates and the effective rates of their existing FDs, after taking into account the early withdrawal penalty,” Kukreja explains.

Laddering deposits

As we are close to peak rates, at some point rates may reverse. There is therefore little scope for obtaining higher returns by raising rates. “If you start creating an FD ladder now, you run the risk of lowering rates, which won’t be a good outcome for you. Therefore, it makes more sense at peak rates to lock into the FD durations longer available. Every time you see FD rates go up, you can always liquidate some of your FD and reinvest for higher returns,” says Shetty.

Bank deposits up to Rs 5 lakh are insured under the Deposit Insurance Credit Guarantee Scheme (DICGC), a subsidiary of RBI. Even small financial banks are also classified as regular banks and their depositors are covered by DICGC. The insurance covers each depositor of each scheduled bank for cumulative deposits (including fixed, current, savings and recurring deposits) up to Rs 5 lakh, in the event of bank failure.

Thus, depositors seeking higher yields but with the highest possible capital protection features should spread their high-yield FDs across multiple scheduled banks in such a way that their cumulative deposits with each of these scheduled banks do not not cross the limit of Rs 5 lakh.

Also read: Are deaths by suicide covered by life insurance policies?

PRESS PAUSE

* Most banks currently offer fixed deposits with interest rates of 7% or higher

* The FD portfolio must be distributed between banks and various companies and between mandates

* Bank deposits up to Rs 5 lakh are insured under the Deposit Insurance Credit Guarantee Scheme